The sustainability investment landscape in 2026 is fundamentally different from 2025. Geopolitical fragmentation is widening, policy uncertainty is rising, and markets are increasingly moving on their own momentum rather than policy support alone. This year marks the sharpest gap yet between rhetoric and reality, with some governments retreating from climate commitments while others strengthen regulation and enforcement.

For investors, the message is clear: policy is shifting from aspirational to mandatory. Disclosure requirements are tightening. Carbon pricing is going global. And the competitive advantage belongs to those who can navigate policy complexity while identifying opportunities that work regardless of political winds.

This guide covers the policy trends reshaping capital flows in 2026 and the investment opportunities emerging from this transformation.

What This Guide Covers

-

- Policy mechanisms: Carbon pricing, disclosure mandates, taxonomies, and transition finance frameworks

- Sectoral opportunities: Renewable energy, hydrogen, hard-to-abate industries, and circular economy

- Regional landscapes: US, EU, India, China, UK, and Africa's distinct policy trajectories

- Investment implications: How to assess policy risk and identify alpha opportunities

- 2026 specific milestones: Critical dates and deadlines affecting investment decisions

The Global Policy Landscape in 2026

Geopolitical Fragmentation vs. Market Momentum

2026 marks a critical turning point. The consensus that drove the Paris Agreement era is fracturing. Governments face competing priorities: climate action vs. economic growth, energy security vs. emissions reduction, and national sovereignty vs. global coordination.

Yet markets are not waiting. Despite policy headwinds in some regions, capital continues flowing toward commercially viable transition technologies. Physical climate risk is being priced in by prudential regulators. And corporate decarbonization targets are shifting from voluntary pledges to legal obligations backed by enforcement mechanisms.

Policy Divergence by Region

The US is retreating at the federal level while states advance their own climate agendas. California's disclosure laws and New York's climate targets are creating de facto national standards despite federal rollback. The IRA remains in place, though subject to regulatory scrutiny.

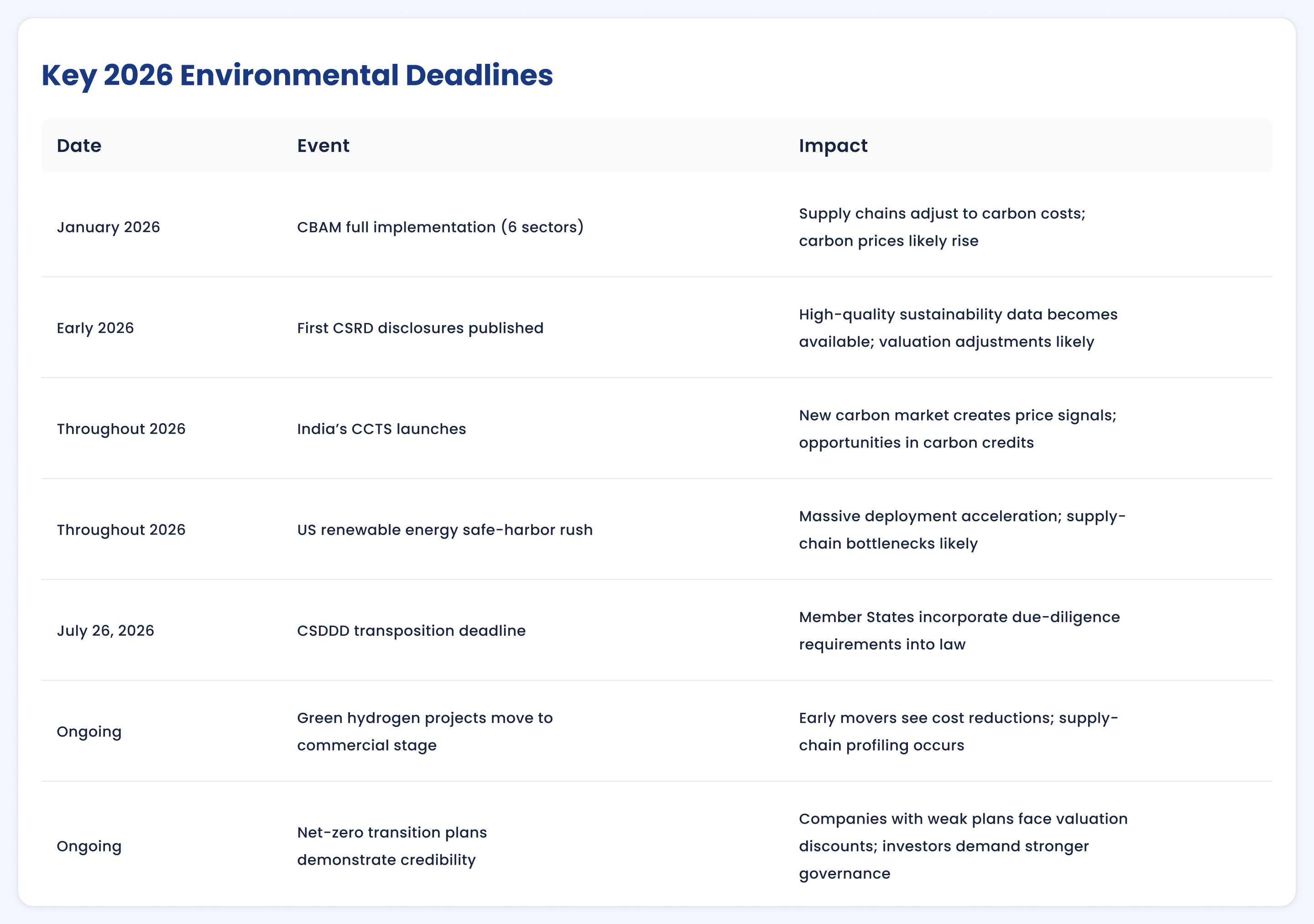

The EU is tightening requirements through the CSRD and CSDDD, with implementation delays (pushed back to ease compliance) and more detailed requirements when they apply. CBAM begins full enforcement in January 2026, reshaping global supply chains and carbon pricing fundamentals.

The Asia-Pacific region is rapidly advancing, driving innovation and opportunities! India's Carbon Credit Trading Scheme launches in 2026. China continues expanding its national carbon market. Vietnam and Indonesia are advancing green transitions through blended finance partnerships.

Key Macro Drivers

Energy security pressures: The energy crisis in Europe and global focus on grid stability are driving investment into grid-balancing renewables and energy storage, not just generation.

Physical climate impacts accelerating: Extreme weather events are no longer theoretical risks. Insurance companies are repricing premiums. Infrastructure investors are demanding climate-proofing standards. Asset owners are measuring physical exposure.

AI energy demand explosion: Data center growth is creating unprecedented electricity demand, driving both renewable energy investments and urgency around energy efficiency.

Carbon Pricing: The Global Architecture Emerges in 2026

EU's Carbon Border Adjustment Mechanism Goes Live

January 2026 marks the full implementation of CBAM on six carbon-intensive sectors: steel, aluminum, cement, fertilizers, electricity, and hydrogen. This isn't theoretical—companies are now facing financial penalties on EU imports.

What this means: Exporters are racing to secure EU carbon credits or implement domestic carbon pricing. Global steel companies are recalculating cost structures. Supply chain sourcing decisions are being revisited based on carbon intensity.

For investors: The spread between high-emission and low-emission producers will widen. European and Korean steel companies with lower emissions face competitive advantages. Emerging-market cement and steelmakers face margin pressure unless they decarbonize rapidly.

Article 6 Carbon Markets Acceleration

The Paris Agreement's Article 6 international carbon credit mechanism is now operational. Countries can trade emission reductions bilaterally (Article 6.2) or through a centralized mechanism (Article 6.4).

This is transformative because: Developing countries can generate revenue from emissions reductions. Developed countries can offset domestic reductions. Global carbon prices begin to converge. Project-level carbon credits gain credibility.

2026 catalysts: India will implement its Carbon Credit Trading Scheme (CCTS), creating a massive new carbon market. Brazil, Colombia, and Vietnam are accelerating ETS development. Article 6 pilot projects are scaling.

Investment angle: Carbon credit prices will rise as supply tightens and demand from CBAM compliance increases. Emerging market carbon credits and nature-based carbon projects are becoming increasingly valuable.

Global ETS Coverage Expanding

Across the world, 38 emissions trading schemes now cover nearly one-fifth of global emissions. China's national market is expanding beyond power generation to include cement and steel. India's launch will add another tier. Mexico's ETS is moving into the implementation phase.

Convergence trend: Countries are harmonizing ETS designs to reduce arbitrage opportunities and create interoperable carbon markets. This raises carbon prices globally and tightens compliance requirements.

Carbon Tax Alternatives Growing

While carbon pricing remains politically challenging in some regions, alternative mechanisms are emerging: production taxes, feebates, and efficiency standards. Canada's carbon tax is increasing. The UK is planning carbon tax alternatives if the ETS reforms. These alternatives create similar investment incentives but may have different compliance pathways.

Mandatory Climate Disclosure: 2026 Marks the Shift from Rules to Reality

-

CSRD Rollout Timeline Adjusted—But Requirements Remain Strict

The EU's Corporate Sustainability Reporting Directive was delayed, but 2026 remains a critical year. The first wave of companies (large, public-interest entities) will begin reporting under CSRD for fiscal years 2024-2025, with disclosure in early 2026.

What changed: Implementation dates were delayed by 1-2 years to allow time for guidance development. However, the disclosure requirements themselves are only slightly simplified, and enforcement is being strengthened.

For investors: Expect much higher-quality sustainability data starting in 2026. Double materiality assessments will force companies to identify financially material sustainability risks and opportunities. Scope 3 emissions reporting will become mandatory for all large companies within the CSRD scope.

CSDDD Due Diligence Enforcement Begins

By 2026, Member States must transpose the Corporate Sustainability Due Diligence Directive into national law (deadline July 26, 2026). This means companies will face legal liability for supply chain impacts—environmental and social.

Practical impact: Large companies begin formal due diligence processes. Supply chain audits intensify. Emerging market suppliers face pressure to provide detailed environmental and social data. Companies implement technology solutions for supply chain monitoring.

Investment implications: Suppliers with transparent, audited ESG data command premium valuations. Supply chain software providers see surging demand. Companies with weak supplier relationships face material compliance risks.

IFRS Sustainability Standards Adoption Spreads

IFRS S1 and S2 standards are becoming the global baseline for sustainability reporting. Securities regulators in 50+ jurisdictions are signaling adoption. Even the US, despite delays to SEC rules, is seeing institutional investors demand IFRS-aligned data.

2026 reality: Companies targeting institutional investors will adopt IFRS standards regardless of local regulations. This creates de facto global disclosure harmonization.

Scope 3 Emissions Becomes Mandatory for Large Companies

Scope 3 (supply chain emissions) is no longer optional. CSRD, CSDDD, and investor pressure all demand it. This is a game-changer because Scope 3 typically represents 80-90% of a company's total emissions.

Challenges and opportunities: Companies scramble to gather supply chain data. Technology providers offering Scope 3 calculation tools see explosive growth. Suppliers with low-emission operations gain a competitive advantage. Emission reduction opportunities shift from operations to supply chains.

Climate Risk Disclosure: Central Banks and Regulators Enforce

Central Bank Stress Testing Goes Live

Prudential regulators—central banks and banking supervisors—are embedding climate risk into capital adequacy frameworks. The European Central Bank is conducting detailed stress tests. The UK PRA is requiring climate risk disclosures from financial institutions. The US Federal Reserve is following.

What this means: Banks must assess how climate risks and transition policies affect their portfolios. They must hold more capital for climate-exposed assets. They begin reducing exposure to stranded assets and high-emitters.

Capital flow impact: Credit becomes easier and cheaper for low-carbon businesses, harder and more expensive for high-emitters. This acts as a shadow carbon price, reinforcing market signals.

Physical Risk Assessments Become Routine

Asset owners are now required to assess physical climate risk—flooding, heat stress, drought, hurricanes—on their portfolios. This isn't speculation; it's insurance and capital adequacy requirements.

2026 trend: Companies publish detailed physical risk disclosures. Real estate valuations adjust downward in high-risk areas. Infrastructure projects in vulnerable regions face higher financing costs. Climate insurance premiums skyrocket in risky areas.

Investment strategy: Geographic diversification away from physical risk zones. Infrastructure resilience upgrades become value creation levers. Water utilities and flood mitigation technologies see increased investment.

Sustainable Finance Taxonomies: Gatekeeping Capital

EU Taxonomy Enforcement Tightens

The EU Taxonomy is the world's most detailed classification system for sustainable activities. Companies must disclose their alignment with it. Investors use it to screen portfolios. Financial institutions must report taxonomy-aligned lending and investment.

2026 developments: Enforcement mechanisms activate. Non-aligned reporting faces penalties. Companies begin reclassifying activities based on refinements to technical screening criteria. Debate intensifies around transition activities vs. green activities.

Practical implication: Companies must audit their activity classifications. Some activities previously considered "green" may need reclassification. Transition finance becomes a distinct asset class.

Global Taxonomies Proliferate and Converge

India launched its Climate Finance Taxonomy in 2024. ASEAN is developing a common framework. Canada has a green and transition taxonomy. The UK created its own. South Africa is developing one.

Convergence trend: These taxonomies are gradually aligning with EU standards, creating de facto global definitions of green and transition finance.

Investment strategy: Understanding taxonomy alignment across jurisdictions becomes critical. Multi-jurisdictional companies must navigate different definitions. Taxonomy alignment becomes a competitive differentiator.

Greenwashing Crackdown Intensifies

Regulators are now actively prosecuting greenwashing—false or misleading sustainability claims. The SEC sued several companies. European authorities are tightening disclosure verification requirements. Third-party assurance providers are gaining importance.

Impact on capital: Credible, audited sustainability disclosures command premium valuations. Greenwashing risks become material financial risks.

Net-Zero Commitments: From Pledges to Legally Binding Plans

Corporate Transition Plans Become Mandatory Under CSRD

Companies must now disclose detailed transition plans that show how they will achieve their net-zero commitments. These aren't voluntary—they're legally required disclosures under CSRD.

What makes a credible plan: Science-based interim targets (especially 2030). Detailed investment plans. Governance and accountability mechanisms. Clear pathways for hard-to-abate sectors.

Investor scrutiny: Institutional investors are voting against companies with weak transition plans. Asset managers are using the credibility of transition plans as an engagement and stewardship lever. Companies with vague plans face valuation discounts.

Science-Based Targets Initiative (SBTi) Standard Evolves

The SBTi net-zero standard is now the globally recognized framework for corporate climate targets. Companies setting targets without SBTi validation face investor skepticism.

2026 focus: 2030 interim targets become critical. Most companies must show measurable progress by 2026-2027 or face credibility challenges. Capital allocation toward companies meeting interim targets accelerates.

Board Accountability Mechanisms Strengthen

Executive compensation increasingly ties to ESG and decarbonization targets. Board compensation committees must justify pay decisions. Climate expertise is becoming a requirement for director qualifications.

Governance trend: Companies with weak climate governance see rising director liability insurance costs. Climate-literate boards command higher valuations.

Sectoral Decarbonization Policies: Opportunity Hotspots in 2026

Renewable Energy: Safe Harbor Rush and Supply Chain Resilience

The US Inflation Reduction Act created a "safe harbor" window—projects beginning construction before June 16, 2025, benefit from grandfather provisions. 2026 brings new thresholds: projects starting in 2026 must meet 50% domestic content for solar (35% offshore wind).

2026 dynamics: Massive pipeline shift as developers race to start projects under favorable terms. Supply chain pressures intensify. Component sourcing becomes critical. Domestic manufacturing accelerates.

Investment theme: Renewable energy developers with secure supply chains and accelerated deployment capabilities will outperform. Battery storage investors benefit from storage-paired solar investments. Grid modernization becomes essential.

Green Hydrogen: National Missions Launch Investment

India's National Green Hydrogen Mission is moving into full implementation. Phase I (2023-2026) focuses on refining, fertilizers, and city gas sectors. Investment opportunities are emerging in electrolyzer manufacturing, renewable power procurement, and infrastructure development.

The EU's green hydrogen targets under REPowerEU require massive private investment. Japan and South Korea are scaling up hydrogen production. Australia is developing export capacity.

2026 catalysts: Production incentives clarify. Offtake agreements begin closing. Pilot projects move to commercial scale. First-generation electrolyzers reach market competitiveness.

Investment opportunity: Electrolyzer manufacturers. Green hydrogen developers. Related infrastructure (storage, transport, end-use conversion). Long-term is bright, but near-term projects face execution risk.

Hard-to-Abate Sectors: Carbon Contracts for Difference Expand

Steel, cement, and chemicals face the highest decarbonization costs and policy support. Carbon Contracts for Difference (CCfD)—which guarantee revenue certainty for low-carbon producers—are expanding in the EU and being piloted elsewhere.

Mechanics: If carbon prices don't reach a strike price, the government pays the difference. If they exceed it, the company pays back. This de-risks capital investment in decarbonization.

2026 roll-out: First wave of CCfD contracts will be awarded. European industrial companies will begin retrofitting for low-carbon production. Emerging market companies will face pressure to follow or lose market access.

Investment implication: European steel and cement companies with capital for decarbonization retrofits will gain market share. Those without will face margin compression.

CCUS Investment Pipeline: Policy Clarity Improves Economics

Carbon Capture, Utilization, and Storage (CCUS) remains expensive but is becoming more viable with policy support. US tax credits (Section 45Q) were expanded. EU ETS creates financial incentives. Infrastructure is developing.

Reality check: CCUS is still an early-stage technology. Capital costs remain high. Permanent storage regulations are complex. But the policy trajectory is clear—CCUS will be necessary for net-zero pathways.

2026 focus: Demonstration projects move toward commercial viability. Direct air capture costs continue declining. Industrial capture for utilization (chemicals, beverages) becomes economic at scale.

Transport Electrification Accelerates

Electric vehicle mandates are tightening globally. The EU requires zero-emission new cars from 2035. China dominates EV production. The US IRA incentivizes EV adoption.

2026 trend: Used EV markets emerge. Charging infrastructure races to keep up with adoption. Battery supply chains face material constraints and price pressures.

Investment strategy: EV charging infrastructure. Battery recycling and second-life applications. Automotive supply chains are transitioning to EV components.

Circular Economy Policies Reshape Material Flows

Extended Producer Responsibility (EPR) requirements are forcing companies to take back and recycle products. The EU's Digital Product Passport is coming. Waste-to-resource programs are scaling.

2026 implications: Product design must now account for end-of-life recycling. Material supply chains shift from virgin extraction to recycled inputs. Waste management becomes a value creation center.

Nature-Based Solutions and Biodiversity Finance

TNFD Disclosure Framework Uptake Accelerates

The Taskforce on Nature-Related Financial Disclosures (TNFD) framework is gaining regulatory adoption. The EU's biodiversity strategy links nature risk to financial stability. Investors are demanding nature risk assessments.

TNFD mechanics: Companies use the LEAP framework (Locate, Evaluate, Assess, Prepare) to identify nature-related risks and opportunities. First disclosures are underway.

2026 reality: Nature risk becomes material for investors with exposure to agriculture, forestry, fisheries, or water-intensive sectors. Companies without nature assessments face valuation discounts.

Global Biodiversity Framework: Nature Credit Markets Emerge

The Kunming-Montreal Global Biodiversity Framework established targets, including protecting 30% of land and ocean by 2030. This is driving massive investment in conservation and restoration.

Nature credits (similar to carbon credits) are becoming tradable. Companies can offset their environmental impact through habitat restoration or protection investments.

Emerging market opportunity: Countries rich in biodiversity can monetize conservation through credit sales. Brazil, Indonesia, and countries in the Congo Basin are exploring this. Investment capital is flowing.

Deforestation Regulations: Supply Chain Reckoning

The EU's Deforestation Regulation (EUDR) requires companies to prove that commodities (soy, palm oil, cattle, cocoa, coffee, rubber, wood) don't come from deforested land. This creates an enormous compliance burden and supply chain disruption.

2026 impacts: Commodity prices rise as supply tightens. Companies face costly supply chain audits. Smallholder farmers in developing countries need support or lose market access. Investment in supply chain traceability technology surges.

Just Transition: Social Equity in Decarbonization

Just Energy Transition Partnerships (JETPs) Scale

JETPs are blended finance structures helping coal-dependent regions transition. South Africa's JETP mobilized $8.5 billion. Indonesia and Vietnam have follow-on programs. These signals development banks' commitment to equitable transitions.

Structure: Concessional finance from developed countries funds clean energy capacity while supporting worker and community transition programs. Private capital follows as risk is reduced.

2026 expansion: More JETPs will be announced. Capital deployment accelerates on existing programs. Impact investing follows JETP-backed projects.

Worker and Community Protection Mechanisms Strengthen

Regulations now require worker engagement and community benefit agreements in decarbonization projects. Skills development programs are mandatory. "Just transition" is no longer voluntary.

Investment implication: Projects with strong community engagement and worker support face lower social risk and faster permitting. Those without face delays and opposition.

Energy Affordability and Access in Emerging Markets

As energy systems transform, ensuring access and affordability for low-income populations becomes critical. Policy focus is shifting from just energy access to just energy transition—protecting those dependent on fossil fuels.

2026 reality: Emerging market decarbonization programs include affordability safeguards. Renewable energy projects prioritize local employment. Energy efficiency programs target low-income households.

Climate Finance Mobilization

Blended Finance Mechanisms Scale Rapidly

Blended finance—combining concessional public capital with commercial private capital—is the fastest-growing climate finance tool. Development finance institutions are deploying hundreds of billions through blended structures.

Why it works: Public capital (often from aid budgets) absorbs first-loss risk, improving risk-return profiles for private capital. This unlocks capital that wouldn't otherwise flow to emerging markets and early-stage technologies.

2026 catalysts: The IMF's Resilience and Sustainability Trust is scaling. The Global Green Bank network is expanding. First-loss funds are multiplying across sectors and regions.

Investor strategy: Participate in blended finance funds. Deploy capital in senior tranches where public first-loss capital de-risks investment. Target 7-10% returns with lower risk than standalone climate investments.

Green Bonds and Sustainability-Linked Instruments

Green bond issuance hit record levels in 2024-2025. Sustainability-linked bonds (whose coupon adjusts based on ESG targets) are emerging. Transition bonds are becoming mainstream.

2026 trends: Issuance continues scaling. Coupon spreads tighten as supply increases. Compliance verification becomes more rigorous. Second-party opinions and certifications are standard.

Emerging opportunity: Sustainable bonds from emerging market issuers. Transition bonds from high-emitting sectors (steel, cement, oil majors transitioning). Green bonds in local currency (reducing FX risk for local investors).

Loss and Damage Finance Gets Real

At COP29, developed countries committed to a Loss and Damage Fund to help vulnerable countries cope with climate impacts. 2026 will see the initial deployment of funds to frontline countries and communities.

Significance: This is distinct from mitigation and adaptation finance. It acknowledges that some climate impacts can't be prevented, and funds will support recovery and resilience.

Investment angle: Adaptation infrastructure that prevents loss and damage. Disaster insurance products. Climate resilience bonds.

Supply Chain Decarbonization and Scope 3 Policies

Scope 3 Emissions Become Competitive Differentiator

As Scope 3 disclosure becomes mandatory, competition intensifies to reduce supply chain emissions. Companies with high-emitting suppliers face valuation discounts.

2026 dynamics: Supply chain engagement accelerates. Suppliers are offered capital support to decarbonize. Technology solutions for emissions calculation proliferate. Transparency becomes a competitive advantage.

Investment implication: Suppliers with low supply chain emissions command premium valuations and easier access to capital. Supply chain software and sustainability consulting see explosive growth.

EU Deforestation and Human Rights Due Diligence

Two major EU regulations are forcing companies to transform supply chains:

- Deforestation Regulation: Prove commodities don't drive deforestation.

- Corporate Sustainability Due Diligence Directive: Identify and mitigate environmental and social harms.

2026 compliance reality: Audits become standard. Smallholder farmer programs emerge. Supply chain costs rise initially as compliance infrastructure is built.

Sustainable Procurement Standards

Governments and large companies are embedding sustainability requirements into procurement. This cascades through supply chains and drives systemic change.

Market effect: Sustainable suppliers expand capacity and invest in efficiency. Unsustainable suppliers lose market access. Price premiums for sustainable goods narrow as scale increases.

Physical Climate Risk Integration into Finance

Insurance Sector Repricing Accelerates

Climate-related insurance losses are hitting records. Insurers are repricing premiums to reflect the increased frequency and severity of events. Coverage in high-risk zones is being curtailed.

2026 impact: Property and casualty insurance becomes unaffordable in certain regions. This is forcing infrastructure and real estate investors to prioritize climate-resilient locations.

Opportunity: Catastrophe bonds and parametric insurance products. Infrastructure hardening and resilience upgrades. Climate-adapted agriculture and forestry.

Infrastructure Climate-Proofing Mandates

Regulators and lenders now require infrastructure projects to be climate-proofed—designed to withstand future climate conditions. This adds a high upfront cost but reduces operational risk.

2026 requirements: All major infrastructure projects factor in climate scenarios. Utilities invest in grid resilience and redundancy. Transportation networks are hardened against flooding and heat stress.

Adaptation Finance Opportunities Surge

While mitigation (emissions reduction) has dominated climate finance, adaptation is gaining urgency. Vulnerable countries need capital for adaptation infrastructure.

2026 catalysts: Loss and Damage Fund deployment. Adaptation bond issuance increases. Adaptation projects in developing countries are attracting private investment.

Technology and Innovation Policy Support

AI and Climate Solutions Acceleration

AI is accelerating climate solutions: optimizing renewable energy grids, improving climate modeling, detecting physical hazards, and monitoring supply chains. Governments are supporting AI-for-climate initiatives.

2026 focus: Data center energy efficiency mandates drive renewable energy investment. Climate AI startups attract venture capital. Emission calculation AI becomes a standard tool.

Production-Linked Incentives (PLI) Expand

Countries are using PLI schemes to localize clean energy manufacturing. India's PLI for batteries and solar. The US IRA tax credits for domestic manufacturing. The EU's measures for green tech.

2026 expansion: More countries adopt PLI schemes. Component and equipment manufacturing capacity grow. Supply chain resilience improves, but at a higher initial cost.

Demonstration Project Funding

Governments fund first-of-a-kind (FOAK) technology demonstrations to reduce risk for private deployment. Direct air capture, green hydrogen, advanced energy storage, and sustainable aviation fuels are advancing through demonstration programs.

2026 activity: Projects move from pilot to commercial demonstration. Some hit market viability milestones. Failed experiments are discontinued, freeing capital for the next generation.

Regional Policy Deep Dives: Where the Action Is in 2026

United States: IRA Deployment and Policy Uncertainty

The Inflation Reduction Act remains the most extensive climate investment package in history: $369 billion in climate spending through 2032. However, the political environment is uncertain.

2026 realities:

-

- Safe harbor projects: Massive acceleration of renewable energy projects starting in 2026 to lock in favorable terms.

- Domestic content rules: 50% domestic content requirements for solar in 2026 (up from 45% in 2025).

- Supply chain pressures: Foreign entity of concern (FEOC) sourcing restrictions tighten, pressuring supply chains.

- State-level leadership: California's climate disclosure laws (SB 253, SB 261) become a de facto national standard.

- Federal uncertainty: Political changes create policy risk but don't immediately change enacted law.

Investment strategy: Deploy capital into safe-harbor renewable projects in 2026. Source equipment domestically to meet domestic content requirements. Position in battery and component manufacturing in US-friendly jurisdictions.

European Union: Regulation Tightens, Investment Accelerates

The EU is doubling down on climate regulation despite competitiveness concerns. CSRD, CSDDD, and CBAM are all advancing in 2026.

Critical 2026 dates:

-

- January: CBAM full implementation on six sectors

- July 26: Member States transpose CSDDD into national law

- Throughout: First wave of CSRD disclosures published by March 2026

Key policies shaping investment:

-

- Fit for 55 Package: EU emissions reduction target tightened to 61% by 2030 (vs 2005)

- REPowerEU: Green hydrogen and renewable energy acceleration to reduce energy dependence

- EU Green Deal Industrial Plan: Subsidy competition with the US IRA

- Climate Bank Roadmap Phase 2 (2026-2030): €1 trillion mobilization target

Investment opportunity: European renewable energy and green hydrogen. Circular economy businesses. Companies with credible transition plans. Infrastructure hardening and adaptation.

India: Carbon Market Launch and Sunrise Sector Investment

India's National Green Hydrogen Mission is moving into implementation. The Carbon Credit Trading Scheme is launching in 2026. State governments are releasing green hydrogen policies.

2026 catalysts:

-

- CCTS launch: Trading of carbon credits begins, creating price signals for emissions reduction

- Green hydrogen hubs: Phase I focus (refining, fertilizers, city gas) sees first commercial projects

- State-level policies: Six states plus more in the pipeline release hydrogen policies, creating regional opportunities

- Viability gap funding: Government support de-risks early green hydrogen projects

- Production-linked incentives: Electrolyzer and renewable energy component manufacturing capacity grow

Investment strategy: Green hydrogen in fertilizer and refining sectors. Carbon credits in India. Electrolyzer and component manufacturing. State-specific renewable energy zones. Note: Near-term returns are limited; long-term potential is significant.

China: National Carbon Market Expands, Industrial Transition Accelerates

China's national carbon market launched in 2021, initially covering only the power sector. 2026 will see expansion to cement and steel—China's highest-emitting sectors.

Policy direction:

-

- Dual carbon goals: Peak 2030, neutral 2060, drive sustained investment in renewables and electrification

- ETS expansion: Cement and steel entry will create ~1.5 billion tons of additional covered emissions

- Industrial green upgrades: Mandated emission reductions drive technology adoption

- Article 6 engagement: China is active in international carbon markets

Investment perspective: Chinese renewables and energy storage. Equipment and technology suppliers to industrial decarbonization. Carbon credit opportunities. Be aware of geopolitical risks and market access restrictions.

United Kingdom: Climate Bank Expansion and Transition Plan Requirements

The UK is maintaining its climate ambition despite leaving the EU. The UK Green Bank is evolving into a climate investment vehicle.

2026 landscape:

-

- Transition Plan Taskforce (TPT) expectations are embedded across the financial system

- Climate Bank expansion: Increasing deployment of concessional capital alongside private investment

- Mandatory transition disclosures: Companies must disclose credible transition plans

- Regulated water sector capex: Major investment in water efficiency and resilience through regulated returns

Opportunity: UK water utilities. Infrastructure resilience and climate adaptation. Companies with credible transition plans. Green bonds and sustainability-linked debt.

Africa and Emerging Markets: JETPs and Blended Finance

Emerging markets are the frontier for climate investment, but capital availability is constrained.

2026 focus:

-

- Just Energy Transition Partnerships: South Africa, Indonesia, Vietnam programs deploy capital

- Blended finance mechanisms: Public first-loss capital attracts private capital to frontier sectors

- Renewable energy expansion: Massive investment needed to meet growing electricity demand sustainably

- Grid and storage: Energy storage becomes critical for high-renewable grids

- Agricultural adaptation: Climate-smart farming and resilience

Investment angle: Blended finance funds targeting emerging markets. Renewable energy in high-growth regions. Agricultural technology and adaptation. Note: Execution risk is high, returns are long-term, but alpha opportunities are significant.

How Investors Should Respond to 2026 Policy Trends

Policy-Aligned Investment Strategies

- Thematic Investing: Target sectors with clear policy tailwinds and commercial viability

-

- Clean energy transition (solar, wind, storage, grid tech)

- Green hydrogen and alternative fuels

- Energy efficiency and demand management

- Sustainable agriculture and nature-based solutions

- Circular economy and resource efficiency

- Portfolio Decarbonization: Align holdings with net-zero pathways

-

- Set interim 2030 targets to demonstrate credibility

- Engage companies on transition credibility

- Divest high-emitters without credible plans

- Allocate capital to decarbonizing sectors

- Transition Finance: Identify high-emitters with credible transition plans

-

- Highest alpha opportunity, but execution risk is real

- Look for companies with science-based targets, detailed capex plans, and governance accountability

- Evaluate first-mover advantages in policy-supported technologies

- Monitor policy risk to transition plans

- Emerging Market Opportunities: Deploy blended finance alongside development finance

-

- JETPs and global green banks offer a lower-risk entry

- Emerging market clean energy offers higher returns at acceptable risk

- Nature-based solutions attract growing capital

Risk Management

Policy risk: Political change can alter investment thesis. Scenario analysis and diversification are essential.

Stranded asset risk: High-emitters without credible transition plans face long-term value destruction. This risk accelerates in 2026 with mandatory transition planning requirements.

Physical climate risk: Geographic diversification away from high-risk zones. Infrastructure climate-proofing. Insurance and adaptation strategy.

Execution risk: Green technology companies and emerging market projects carry execution risk. Deal flow and portfolio company monitoring are critical.

Engagement and Stewardship

2026 engagement priorities:

-

- Push companies for credible transition plans (not just targets)

- Demand Scope 3 emissions measurement and reduction strategies

- Vote against weak climate governance

- Engage in supply chain decarbonization

- Monitor physical risk assessments

Conclusion: From Policy Talk to Investment Action

2026 is the year when climate policy crosses from aspirational to mandatory, from rhetorical to financial. Disclosure becomes law. Carbon pricing becomes global. Transition plans become investment criteria. Physical risk becomes material.

For investors, this creates both risk and opportunity. Risk for those holding high-emitters without credible transition plans or exposed to physical climate hazards. Opportunity for those positioned in policy-supported sectors, emerging market clean energy, nature-based solutions, and enabling technologies.

The winners in 2026 and beyond will be those who:

- Read policy signals and position capital ahead of enforcement

- Assess transition credibility and invest in companies with executable plans

- Diversify geographically to hedge policy risk

- Engage actively to shape corporate and policy outcomes

- Think long-term while managing near-term policy uncertainty

The policy landscape in 2026 is complex and geographically fragmented. But the underlying trend is clear: climate policy is becoming financial policy. The transition to net-zero economies is permanently reshaping capital allocation.

Additional Resources for 2026 Policy Research

Key Organizations and Reports to Monitor

- MSCI Sustainability Research: Quarterly trends and data

- S&P Global Sustainable1: ESG trends and analysis

- World Economic Forum: Industry transition reports

- Bloomberg NEF: Climate finance and clean energy data

- Climate Policy Initiative: Policy analysis and deep research

- UNEP FI: Sustainable finance guidance and initiatives

- Transition Pathway Initiative: Company transition assessments

2026 Policy Calendar

- UNFCCC subsidiary bodies meetings (June, October)

- COP31 (November 2026, host TBD)

- National climate announcements (varies by country)

- Renewable energy auction results (ongoing)

- Corporate sustainability reporting disclosures (ongoing)

Investment Frameworks for 2026

- Net Zero Investment Framework (NZIF)

- Task Force on Climate-Related Financial Disclosures (TCFD)

- Corporate Sustainability Reporting Directive (CSRD)

- IFRS Sustainability Standards (S1, S2)

- Science-Based Targets Initiative (SBTi) Net-Zero Standard

- Taskforce on Nature-Related Financial Disclosures (TNFD)

Frequently Asked Questions (FAQ)

1. How does CBAM impact my investment portfolio?

CBAM increases costs for importing carbon-intensive goods into the EU. For investors, this creates winners and losers: low-emission producers gain competitive advantage (premium valuation), high-emitters face margin compression. Diversify away from high-emission concentrated industries without transition plans.

2. What's the difference between green finance and transition finance?

Green finance funds activities that are already low-emission or low-impact (solar, wind, energy efficiency). Transition finance funds companies or projects that are currently high-emitting but have credible pathways to significant emissions reduction (coal-plant conversion, steel mill retrofits, oil-to-renewables transitions). Transition finance has higher alpha potential but higher execution risk.

3. Which regions offer the best policy support for renewable energy in 2026?

India offers strong support through PLI schemes and renewable energy zones. The US continues IRA benefits but with tightening domestic content rules. The EU provides stable long-term policy through FiT and auction frameworks. Brazil offers high growth potential with blended finance. Consider blending high-return emerging markets with stable-return developed markets.

4. How do I assess policy risk in my decarbonization investments?

Use scenario analysis: (1) accelerated climate policy, (2) status quo, (3) policy retreat. Diversify across geographies with different political systems to hedge policy risk. Monitor governments' fiscal capacity to maintain climate spending. Watch for early warning signs of policy shifts (electoral changes, fiscal constraints, growth pressures).

5. What are the most important 2026 compliance deadlines for companies?

For large companies: CSRD first-wave disclosures (published early 2026). Supply chain due diligence preparation for CSDDD compliance. Transition plan refinement to demonstrate credibility. Scope 3 emissions measurement and reduction strategy development.

For supply-chain-exposed companies: Deforestation compliance audits intensify. Due diligence documentation. Sustainable sourcing proof.

6. How do international carbon markets (Article 6) affect emerging market investments?

Article 6 creates pathways for emerging markets to monetize emissions reductions. This improves investment returns on clean energy and conservation projects. However, it also introduces complexity around carbon credit supply and pricing. Look for projects in countries with transparent carbon credit frameworks and strong governance.

7. Which climate tech sectors offer the best 2026 investment opportunities?

High confidence: Renewable energy deployment (safe harbor rush), battery storage (grid balance), energy efficiency software, AI for emissions management, supply chain transparency.

Emerging opportunity: Green hydrogen (moving from pilot to commercial), direct air capture (demonstrations scaling), sustainable aviation fuel (policy support increasing).

Longer-term: Advanced materials, fusion energy, synthetic biology for decarbonization.

8. How do I invest in just transition alongside decarbonization?

Mechanisms: Just Energy Transition Partnership blended finance funds. Development finance institutions with just-transition mandates. Community benefit agreements in project selection. Skills development and worker support programs.

Returns: JETPs typically offer concessional returns (5-8%) with development impact. Assess program governance, fund management, and execution capability.

9. What role do central banks play in climate policy in 2026?

Central banks are integrating climate risk into prudential regulation, capital requirements, and stress testing. This changes capital flows: credit becomes cheaper for low-carbon businesses, more expensive for high-emitters. Banks reduce exposure to carbon-intensive sectors and physical risk zones. This reinforces market signals and accelerates transition.

10. How can I invest in climate adaptation and physical resilience?

Direct: Infrastructure resilience (hardened utilities, flood control), climate-adapted agriculture, water infrastructure, disaster insurance, and parametric products.

Indirect: Adaptation bonds, resilience funds, green investment banks with adaptation mandates, and development finance institutions.

Emerging: Nature-based solutions (mangroves, wetlands, forests), climate-resilient real estate.

.png)