Introduction to Green Lending

As the world shifts its focus towards sustainability and environmental protection, green lending has emerged as a crucial strategy for banks to support the transition to a low-carbon economy. The Global Green Finance Market Size is expected to reach USD 28.71 Trillion by 2033, at a CAGR of 21.25% during the forecast period 2023 to 2033, based on a report by Spherical Insights.

Green lending involves providing financial products and loans to support environmentally friendly projects and initiatives, such as renewable energy projects, energy-efficient buildings, electric vehicles, sustainable agriculture, and more. This approach aims to direct capital towards activities with a positive environmental impact and help mitigate climate change. Banks that engage in green lending can reap several benefits, including alignment with sustainability goals, reduced risk, a competitive advantage, and growth potential.

To determine if green lending is a good fit for your bank, consider factors such as alignment with your bank's mission and values, market demand, expertise and resources, risk management, and regulatory environment. By evaluating these factors and understanding the various aspects of green lending, banks can position themselves as leaders in sustainable finance and contribute to a greener, more sustainable future for their institutions and communities.

Benefits of Green Lending

Engaging in green lending can offer several benefits for banks:

- Alignment with sustainability goals: Banks can demonstrate their commitment to environmental stewardship and contribute to global sustainability by supporting green projects.

- Reduced risk: Investing in green technologies can help mitigate the risks associated with climate change and environmental degradation.

- Competitive advantage: Banks can attract environmentally conscious customers and investors with green lending products.

- Growth potential: Banks and credit unions that offer green financing could reap the benefits of an escalating market demand.

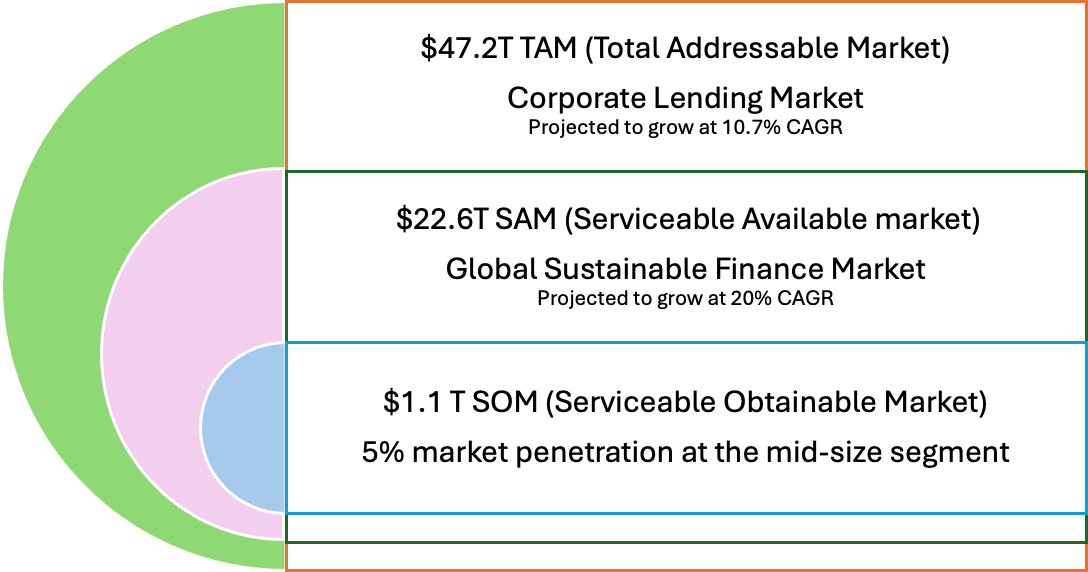

Market Opportunity

Source:

Sustainable Finance Market by Investment Type

Supply Chain Finance Market by Offering

Corporate Lending Market Size, Share & Growth | 2031

Typical Characteristics of Green Lending 101

|

Purpose-Specific |

Green loans are earmarked for environmentally sustainable projects and purchases, ensuring that the borrowed funds are utilized for initiatives that contribute to environmental conservation and sustainability. |

|

Clear Environmental Benefits |

Projects funded by green loans should provide clear environmental benefits, such as renewable energy products, sustainable water management, and green buildings certified to have a positive environmental impact. |

|

Dedicated Account |

Green loans should be credited to a dedicated account to maintain transparency and integrity. This would allow borrowers to track the funds and ensure they are used for green projects. |

|

Reporting Mechanism |

Borrowers of green loans should have readily available information on how the proceeds are used, including a list of green projects funded, the amount allocated, and the expected impact of these projects. This information should be reviewed annually to ensure accountability and transparency. |

|

Alignment with Green Loan Principles |

Green loans should adhere to international standards like the Green Loan Principles, which outline core components such as the use of proceeds, project evaluation and selection process, management of proceeds, and reporting mechanisms to ensure the loan's alignment with environmental objectives. |

|

Environmental Stewardship |

Green loans promote sustainability and environmental stewardship in personal finance, encouraging borrowers to invest in eco-conscious initiatives like energy-efficient home improvements, renewable energy installations, electric vehicles, and other sustainable lifestyle choices. |

Evaluating Green Lending for Your Bank

To determine if green lending is a good fit for your bank, consider the following factors:

- Alignment with your bank's mission and values: Assess whether green lending aligns with your bank's overall mission, values, and strategic objectives.

- Market demand: Evaluate the potential demand for green lending products in your target market and the competitive landscape.

- Expertise and resources: Determine whether your bank has the knowledge, resources, and infrastructure to effectively implement and manage a green lending program.

- Risk management: Assess the potential risks associated with green lending and ensure appropriate risk management strategies are in place.

- Regulatory environment: Stay informed about relevant regulations and guidelines related to green lending and ensure compliance.

Green lending represents a pivotal shift in the financial sector towards supporting sustainable development and addressing climate change. As the global emphasis on sustainability continues to grow, green lending not only offers a pathway for banks to differentiate themselves in the market but also aligns with regulatory trends and investor expectations. However, the successful implementation of green lending requires robust frameworks for measuring and managing both the environmental and financial impacts. By embracing these practices, financial institutions can play a crucial role in fostering a more sustainable future while securing long-term profitability and resilience.

.png)