Measuring the impact of green lending involves a comprehensive assessment of both environmental and financial outcomes to ensure that funded projects align with sustainability goals and offer economic benefits. Key performance indicators (KPIs) for environmental impact include metrics such as reductions in greenhouse gas emissions, improvements in energy efficiency, water savings, and waste reduction.

Financial performance is evaluated through metrics like default rates, return on investment, and overall profitability of green loans. Tools such as environmental impact assessments, carbon accounting, and sustainability reporting frameworks like the Global Reporting Initiative (GRI) and the Task Force on Climate-related Financial Disclosures (TCFD) provide structured methods for tracking and reporting these impacts. Additionally, third-party certifications and audits can enhance credibility and transparency. By effectively measuring and communicating these impacts, financial institutions can validate their contributions to sustainability, attract environmentally conscious investors, and mitigate potential risks associated with greenwashing.

De-risking Green Investments

De-risking means reallocating, sharing, or reducing the existing or potential risks associated with green investment. It refers to the strategies and mechanisms employed to reduce the financial risks associated with lending for environmentally sustainable projects. These instruments encourage more financial institutions to support green initiatives, which might otherwise be perceived as too risky. Here are some common approaches to de-risking green lending:

De-risking means reallocating, sharing, or reducing the existing or potential risks associated with green investment. It refers to the strategies and mechanisms employed to reduce the financial risks associated with lending for environmentally sustainable projects. These instruments encourage more financial institutions to support green initiatives, which might otherwise be perceived as too risky. Here are some common approaches to de-risking green lending:

- Government Guarantees and Incentives

Some governments can provide guarantees to cover potential losses, reducing the risk for lenders. Subsidies, tax breaks, and other financial incentives do make green projects more attractive.

- Public-Private Partnerships (PPPs)

Collaborations between the public and private sectors can distribute risk. Governments and international organizations often co-invest with private entities in green projects, sharing both risks and returns.

- Green Bonds and Green Loans

Issuing green bonds or offering green loans can attract investors specifically interested in sustainable projects. These financial instruments often come with lower interest rates due to the high demand from socially responsible investors.

- Insurance Products

Specialized insurance products can protect against specific risks associated with green projects, such as natural disasters for renewable energy installations.

- Blended Finance

Blended finance involves combining concessional funds from public sources with private capital. This lowers the overall risk for private investors, making it more attractive for them to invest in green projects.

- Technical Assistance and Capacity Building

Providing technical support and capacity building for project developers can improve the quality and feasibility of green projects, thereby reducing the perceived risk for lenders.

- Credit Enhancement

Mechanisms like loan guarantees, first-loss provisions, and subordinated debt can improve the credit profile of green projects, making them more appealing to investors and lenders.

- Risk Assessment and Management Tools

Advanced risk assessment tools and frameworks can help lenders better understand and manage the risks associated with green projects. This includes environmental, social, and governance (ESG) criteria integration.

- Diversification of Portfolio

Lenders can mitigate risk by diversifying their green lending portfolios across different sectors and geographies. This reduces the impact of any single project or market downturn.

- Market Development and Policy Support

Strong regulatory frameworks and policies that promote green investments can reduce uncertainties and risks. This includes setting clear environmental standards, creating carbon pricing mechanisms, and ensuring long-term policy stability.

Some examples of De-risking in Action

- Climate Investment Funds (CIF)

The CIF provides concessional financing to promote investments in renewable energy, energy efficiency, and climate resilience in developing countries. It de-risks investments by blending public and private finance and offering favorable loan terms and guarantees.

- Green Climate Fund (GCF)

The GCF uses public funds to mobilize private-sector investment in climate mitigation and adaptation projects. It offers grants, concessional loans, guarantees, and equity investments to reduce the financial risk of green projects.

- Multilateral Development Banks (MDBs)

Institutions like the World Bank, Asian Development Bank (ADB), and African Development Bank (AfDB) offer various de-risking instruments. For instance, the World Bank's Multilateral Investment Guarantee Agency (MIGA) provides political risk insurance and credit enhancement to green projects.

- European Investment Bank (EIB)

The EIB provides long-term financing for sustainable projects and employs risk-sharing instruments. For example, the EIB's Project Bond Initiative supports large-scale infrastructure projects, including renewable energy, by providing credit enhancement.

- Renewable Energy Performance Platform (REPP)

REPP supports renewable energy projects in sub-Saharan Africa by offering development capital, risk mitigation instruments, and technical assistance. It aims to bridge the gap between early-stage project development and commercial investment.

- UK Guarantees Scheme (UKGS)

The UKGS provides government-backed guarantees to infrastructure projects, including those in the green energy sector. These guarantees reduce financial risk and help attract private investment.

Managed by various financial institutions, these funds blend concessional and commercial finance to de-risk investments in projects that align with the United Nations SDGs, including clean energy and sustainable infrastructure.

- USAID Development Credit Authority (DCA)

USAID's DCA provides partial credit guarantees to mobilize local capital for green projects in developing countries. By covering a portion of the risk, DCA encourages local banks to lend to renewable energy and other sustainable initiatives.

- Green Bonds

Issuing green bonds can lower the cost of capital for green projects. For example, the European Investment Bank's green bonds have financed renewable energy and energy efficiency projects across Europe.

- Risk Mitigation Instruments by Insurance Companies

Insurance products, such as weather risk insurance and performance guarantees, provided by companies like Munich Re and Swiss Re, help manage risks specific to green projects, making them more viable for investors and lenders.

- Blended Finance Platforms

Platforms like Convergence blend concessional capital from public or philanthropic sources with private sector investments to lower the risk and enhance the attractiveness of green projects. This approach has been used in various sectors, including renewable energy, sustainable agriculture, and water management.

Getting Started with Green Lending

Embracing green lending can be a strategic move for CDFIs and credit union banks looking to impact the environment while driving financial growth positively. Banks can position themselves as leaders in sustainable finance by exploring avenues such as real estate financing, green loans, government programs, and emerging trends like agriculture biochar loans and EV charging financing. To assess your bank's readiness for green lending, consider taking our readiness questionnaire (QNR) in the banner and embark on a journey towards a greener, more sustainable future for your institution and community.

Future Direction in Green Lending

The future of green lending is bright, with significant growth expected in the coming years as the world transitions to a more sustainable economy. Here are some key trends and strategies for the future direction of green lending:

- Continued growth in green loans and bonds

Green loans and bonds, which finance environmentally friendly projects, are expected to see sustained growth. According to Refinitiv, the sustainability-linked lending market experienced huge growth in 2021, with a record-breaking US$1.6 trillion in global ESG financing completed. This trend is likely to continue as more investors and borrowers prioritize sustainability.

- Expansion into new sectors

While green lending has traditionally focused on renewable energy, there is growing interest in expanding into other sectors. Green loans are now being used to finance projects like clean transportation, pollution prevention, and sustainable water and waste management. As awareness of environmental issues grows, green lending will likely spread to more industries.

- Increased focus on impact measurement

As the green lending market matures, greater emphasis will be placed on measuring the actual environmental impact of financed projects. Lenders and investors want tangible evidence that their money is making a difference. Developing robust impact measurement frameworks will be crucial for the long-term success of green finance.

- Government support and regulation

The United States has a growing government support and regulation trend promoting green finance. Initiatives such as the National Clean Energy Fund and guidelines from regulatory bodies like the Securities and Exchange Commission (SEC) play a crucial role in fostering the development of green bonds and encouraging Environmental, Social, and Governance (ESG) investing practices. This support is vital for expanding green lending and realizing its impact on sustainable finance initiatives.

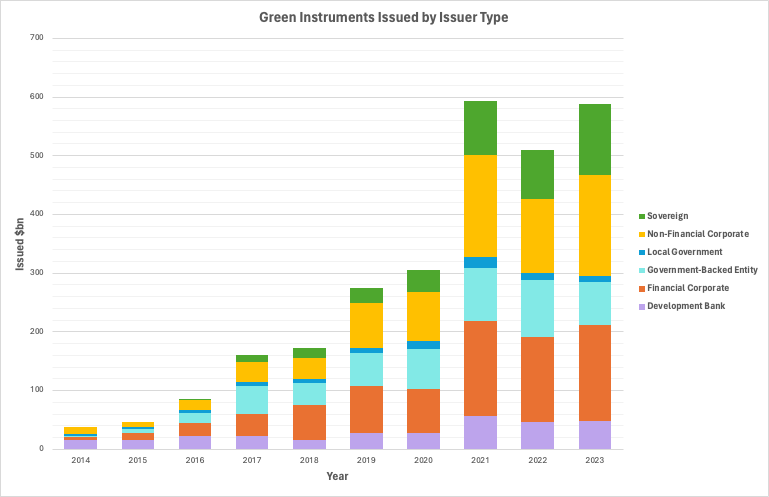

Source: Climate Bonds Initiative

If you decide to pursue green lending, consider the following steps:

- Develop a green lending strategy: Define your bank's objectives, target markets, and product offerings.

- Build internal capacity: Invest in training and development to ensure your staff has the knowledge and skills to support green lending initiatives.

- Partner with experts: Consider collaborating with organizations specializing in green finance to leverage their expertise and resources.

- Communicate your commitment: Promote your bank's green lending initiatives to customers, investors, and other stakeholders to build awareness and trust.

Conclusion

Green lending allows banks to support environmental sustainability while potentially realizing business benefits. By carefully evaluating your bank's capabilities and market conditions, you can determine whether green lending is a strategic fit and develop a plan to implement these initiatives successfully. As the demand for green finance continues to grow, banks that embrace this opportunity may be well-positioned for long-term success.

Some key points to consider in the conclusion:

- Green lending enables banks to align their lending practices with sustainability goals and contribute to environmental protection.

- Engaging in green lending can provide benefits such as reduced risk, competitive advantage, and growth potential for banks.

- Evaluating factors like alignment with the mission, market demand, expertise, risk management, and regulations is crucial in determining if green lending suits a bank.

- Green lending follows the Green Loan Principles to ensure transparency, integrity, and environmental benefits.

- Green lending includes real estate financing (CPACE, PPA), green loans adhering to sustainability standards, and government programs supporting eco-friendly initiatives.

- The future of green lending looks promising, with expected growth in green loans and bonds, expansion into new sectors, increased focus on impact measurement, and government support.

By embracing green lending, banks can position themselves as leaders in sustainable finance and contribute to a greener, more sustainable future for their institutions and communities.

Green lending presents a strategic opportunity for banks to align with sustainability goals, reduce risk, attract new customers, and contribute to a greener future. Banks can determine if green lending is a good fit by carefully considering market demand, expertise, risk management, and regulations.

.png)